Strengthening Europe’s defense: A vision for a robust and innovative future

Recent developments, such as cyber threats, constraints in ammunition production capacity, and the challenge of delivering advanced weapon systems in the right quantity, time, and quality, have highlighted critical vulnerabilities within European defense forces and industries. As Europe navigates a complex geopolitical landscape, marked by growing threats to its territorial integrity and ongoing conflicts at its Eastern borders, it is imperative to reassess and fortify its defense capabilities.

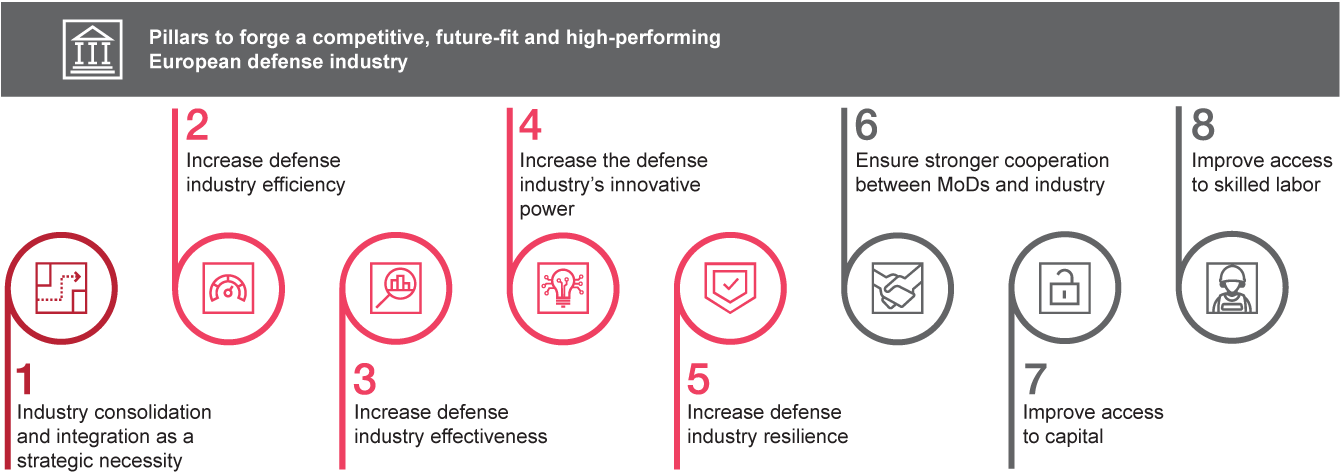

Building a competitive, innovative, and future-ready European defense industry hinges on three essential factors, supported by both the public and private sectors:

- Large-scale investments and higher efficiency and availability of productive capacity (capital, labor, technology)

- An active role for the defense industry in its transformation towards scale, innovativeness, and resilience

- Stronger intrinsic European defense industry collaboration

Our study outlines a comprehensive vision for the necessary transformation of the industry, emphasizing efficiency, effectiveness, innovation, and resilience. This vision is complemented by improved access to production factors and strategic defense industrial policy measure.

Overcoming challenges in Europe’s defense sector

The current geopolitical landscape marks a critical juncture for the defense sectors of Germany and Europe, underscoring the pressing need for adaptation. As technological advancements in both military and civilian sectors accelerate – particularly in areas like artificial intelligence, miniaturization, space exploration, advanced electronics, and cybersecurity – the European defense industry must evolve to keep pace with the changing nature of warfare.

Currently, the following key challenges are still hindering the ability of the German and European defense industries to meet modern warfare demands and fulfill NATO obligations effectively:

- 1.Lack of coordinated procurement: Ministries of Defense (MoD) continue to purchase complex, customized, and nationalized "gold-plated solutions," often lacking a coordinated procurement strategy among European nations

- 2.Outsourcing and slow domestic growth: Following the "peace dividend" era, significant procurement orders have been outsourced internationally, while the domestic defense industry struggles to scale up production

- 3.Limited agility and innovation: The European defense industry’s focus on large-scale system developments has hindered its agility, slowing down rapid innovation cycles

- 4.Fragmented industry and supply chain: Political decisions have resulted in a fragmented industry and supply chain, preventing the realization of economies of scale

- 5.Competitiveness gap: Despite improvements in company and financial performance, a gap persists between European and U.S. defense industries, highlighting a lack of global competitiveness

A roadmap for a competitive, future-fit, and high-performing European defense industry

To enhance the European and German defense industry’s competitiveness, efficiency, effectiveness and resilience, a shift from merely fulfilling public-sector customer orders to assuming greater responsibility within the industry is needed.

Transforming Europe’s defense industry for a secure future

Four key principles can help drive the necessary transformation of the sector towards a competitive, innovative, and future-ready German and European defense industry:

1. A production factor-based, supply-side policy approach is essential. The industry needs to be equipped with the requisite resources: capital, skilled labor, and technology. This foundation is crucial to fostering innovation and maintaining a competitive edge.

2. A focused European Defense Industrial Policy, as recently published by the European Commission, could streamline efforts and challenge the duplication of sovereign defense capabilities and capacities for the sake of national sovereignty and protectionism. This alignment can prevent the inefficiencies caused by weapons systems diversity, which hinders scale and complicates operations and interoperability.

3. Stronger intrinsic European collaboration is vital for survival and growth. This calls for partnerships and joint value creation deals that transcend mere workshare. Recent examples, like the Trinity House Agreement on defense cooperation between the UK and Germany, exemplify the power of collaborative strategies.

4. Active industry-led transformation is essential and needs to include checks and balances within the industry, to prevent profit-focused exploitation of the historic ramp-up in defense budgets. A new modus operandi instead of ‘business as usual’ is required to focus the industry on innovative cycles and new structures for time-to-market efficiency. This includes industry-driven consolidation, focusing on synergies and investing in resilience and efficiency.

Our recommendations prioritize supporting local industries to ensure that public investments benefit regional economies, while maintaining a broad, inclusive perspective. Decision-making should strike a balance between leadership roles and egalitarian values, ensuring that all stakeholders can embrace and adhere to collective decisions. Our primary message is clear: Europe must unite to overcome obstacles and challenges of the 2020s and beyond. The moment for action is now, as the future of European security architecture hinges on the evolution of the European defense industry.

Tobias Müller, Niklas Frings, Lukas Lehmann, Georg Reichel, Sophia Wellek and Penelope Wessel contributed to this report.

This report was crafted in preparation for the Munich Security Conference 2025 (MSC). Concepts and ideas were selected and developed in cooperation with the German Federal Academy for Security Policy (BAKS).

Disclaimer: This report is not an official publication of the MSC. The contents of this paper do not purport to reflect the opinions or views of the MSC and is meant to provide input to and stimulate the debate at the MSC.