{{item.videoDuration}}

{{item.title}}

{{item.text}}

{{item.videoDuration}}

{{item.text}}

Instant payments (IPs) are becoming an increasingly relevant credit transfer method in the European Union (EU) and can play a major role when it comes to expanding the space for account-based payments. Services such as request to pay or mobile wallet solutions with directly linked payment accounts allow money to be withdrawn from accounts and broaden the space for instant credit transfers. In 2021, credit transfers amounted to 24% of the total transaction volume in Europe and represent 94% of the transaction value.

The growth of instant payments will continue in the near future as the European Commission intends to make instant euro payments universally available across Europe. With the aim of preventing fraudulent transactions, detecting errors, and increasing customer trust in instant payments, the proposal includes a requirement for payment service providers (PSPs) to offer a service that enables customers to be notified when a mismatch is detected between the payee’s name and IBAN that the payer provided for the initiation of a payment.

Several IBAN-name check services are already offered by PSPs in several European countries today, and other solutions are in the process of being developed. This reports presents existing IBAN-name check solutions across the Eurozone and strives to cover other relevant market developments related to this topic. It aims to provide helpful information to European PSPs and the entire payments ecosystem as they contemplate how to meet the potential requirement to provide IBAN-name check services at a pan-European level in the (near) future.

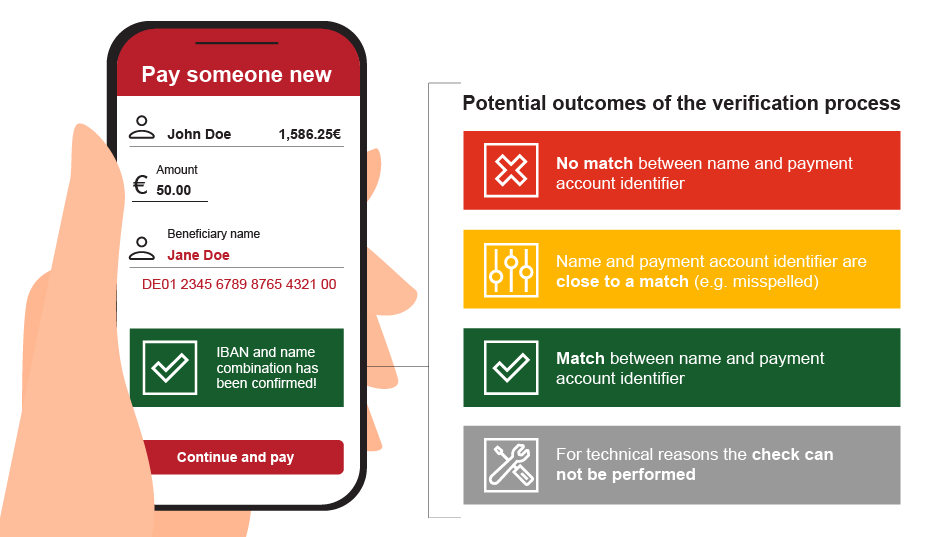

An IBAN-name check allows the payer to verify the validity of the entered combination of a payment account identifier – i.e., the IBAN – and the name of the account holder, as well as the existence of the beneficiary’s account. This check will therefore add an extra layer of trust and security to the payment process.

The functionality of the IBAN-name check could be seamlessly integrated into a PSP’s customer service proposition. It does not interfere with the payment process and is executed before the payment is initiated. It is the understanding of the PSPs interviewed that – whilst it needs to provide a timely response – the IBAN-name check is not part of the execution time of the instant payment itself, which is currently set at a targeted maximum execution time of 10 seconds. Interviews with banks already offering an IBAN-name check have shown that the additional small amount of time needed to perform this check is not detrimental to the instant payment experience.

An IBAN-name check in an online banking environment could potentially work as illustrated below. The payer enters the payment information of the payee and the amount of money they want to transfer. This information is checked in the background in real-time, and the payer receives feedback on the accuracy of the data before authorizing the instant credit transfer.

Improving user trust as well as the possibility of reducing authorized push payment (APP) fraud and misdirected payments were the most frequently discussed topics by the interviewed PSPs and providers in connection with IBAN-name checks.

Real-life experience from banks using the service suggests that fraud is reduced in some of the APP cases. For example, a bank in the Netherlands that introduced the check noted a significant reduction of invoice fraud within the country, i.e., of cases where the fraudster impersonates a creditor, and a migration of fraudulent transactions to the cross-border space. However, some of the banks interviewed stated that fraud reduction rarely happens through the introduction of one single measure and that there might be more effective ways of tackling outgoing payment fraud.

Opinions about the real impact of IBAN-name checks are rather mixed. While some of the interviewed providers are considering broad deployment of IBAN-name check services and see a high potential in these services for fraud prevention, the PSPs interviewed are more cautious. They focus more on customer experience and user feedback than on fraud prevention. Another aspect that was frequently mentioned by interviewed providers and PSPs, is the effort required for their implementation. Again, the picture here is mixed. Banks that already have such a service in place state that the effort for implementation is limited.

The road towards a uniform European IBAN-name check concept has not been finally determined. However, to enable standardization and interoperability, some interviewed PSPs underlined that they would welcome and support the development of a pan-European IBAN-name check concept, ideally by the European Payments Council.

The IBAN-name check has the potential to build trust, rather than offering a silver bullet to combat fraud. The right balance will need to be struck between a wider set of fraud-fighting measures, improvements in user experience, European interoperability, and reasonable implementation efforts.

The authors would like to thank Petia Niederländer, Wolfgang Haunold, Susanne Reich-Rohrwig, Georg Nitsche and Filip Vasic (OeNB), Sebastian Schneider, David Ballaschk and Anne-Sophie Kappel (Bundesbank), Thomas Egner, Annick Moes and Caroline Neyrinck (EBA), as well as Patrick Schnibben and Sarah Luisa Guida (PwC Strategy& Germany) for their contribution.

The co-authorship between Oesterreichische Nationalbank (Austrian National Bank, OeNB), Deutsche Bundesbank (Bundesbank), the Euro Banking Association (EBA), and Strategy& brings together a broad and deep expertise in the field of payments and adjacent topics. To complement this expertise and the targeted desk research carried out for this paper, conversations were held with experts from banks, providers of IBAN-name check services and related institutions.

In total, 17 structured interviews were conducted for the purposes of this paper. Moreover, representatives from nine European banks, based in Austria, Belgium, France, Germany, Italy and the Netherlands, contributed their insights to this exercise.