{{item.videoDuration}}

{{item.title}}

{{item.text}}

{{item.videoDuration}}

{{item.text}}

GCC governments have tried to diversify their economies and reduce their reliance on hydrocarbons in recent years, but the COVID-19 pandemic has exposed important deficiencies in those policies. Although GCC economies have held up relatively well overall, investments in some industries have yielded limited results, and the impact of low oil prices has overwhelmed any potential gains from diversification. As a result, governments need to redouble their efforts in “future-proof” industries such as technology, telecommunications, and health care, and create the right conditions for innovation.

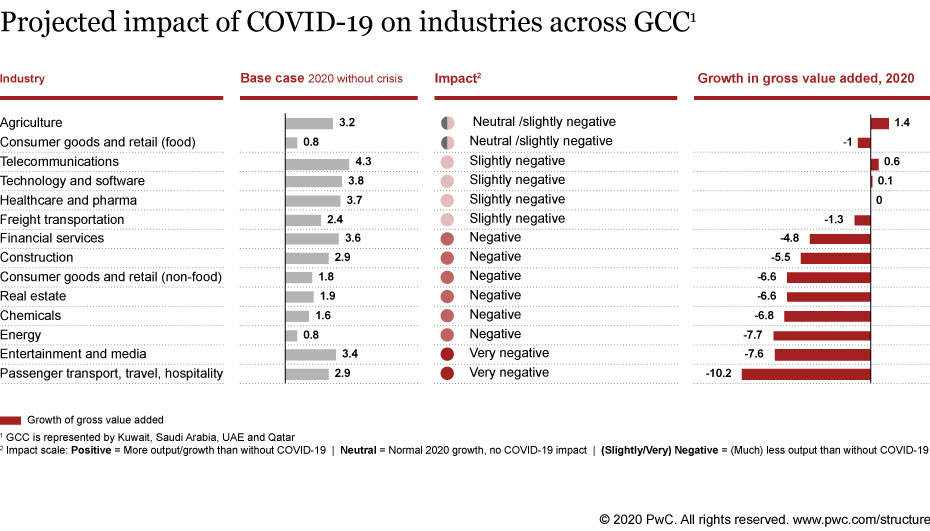

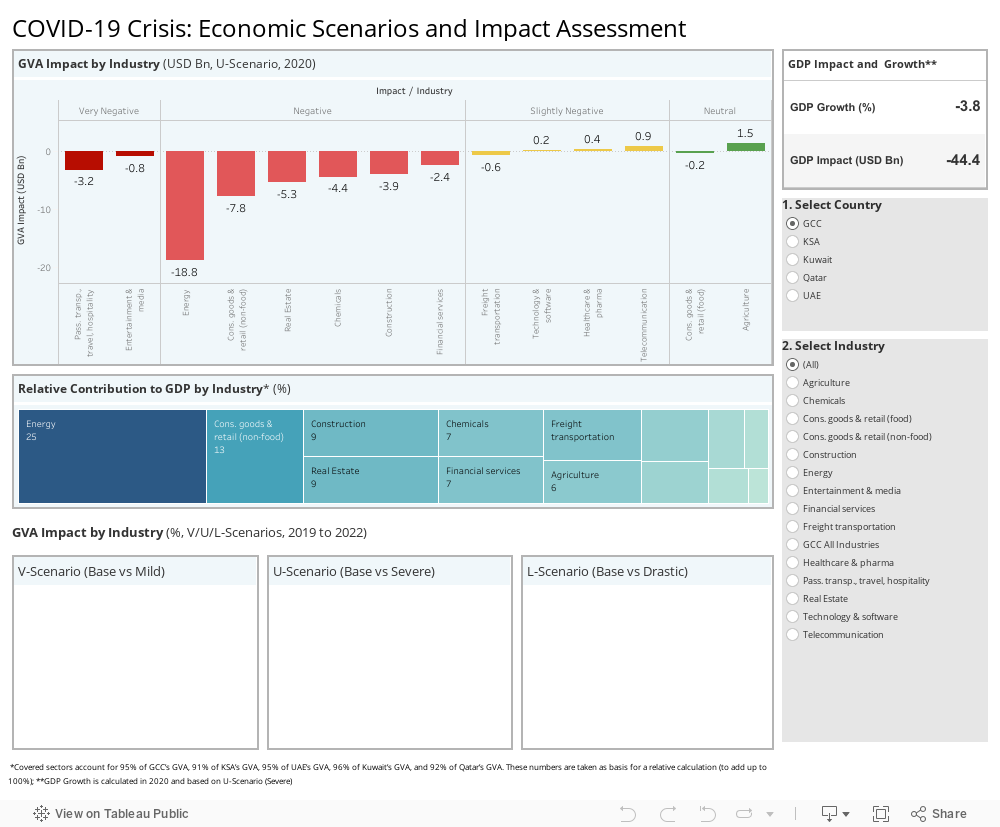

To understand the impact of the dual shock of COVID-19 and lower oil prices, we researched combined quantitative and qualitative inputs for various industries in Kuwait, Qatar, Saudi Arabia, and the UAE with various recovery scenarios. At a macro level, our research suggests that GCC-wide GDP could decline by 3.8% in 2020 under a “middle of the road” scenario. That is smaller than the contractions in the U.S. (-5.4%) and E.U. (-8.6%), thanks in part to swift and substantial intervention by GCC governments.

At the level of individual industries, the story is varied. The industries that will experience the largest declines will be travel and tourism, down 7.4% in 2020, and entertainment and media, dropping 5.6%.

Some sectors are projected to hold up better, such as consumer goods and agriculture. GCC governments have devoted attention and money to job-creating sectors that do not require major investments in R&D and innovation, such as construction, real estate, and retail. Unfortunately, these sectors have been significantly affected by COVID-19 and cannot cushion a projected contraction of 5.2% in the energy sector, which constitutes a significant portion of the economy. In absolute terms, that is a loss of $20 billion of GCC GDP for 2020.

The findings should prompt policymakers to reassess. The dual shock of COVID-19 and lower oil prices have underscored how dependent GCC economies remain on government largesse, which mostly derives from the energy sector. Hydrocarbon resources remain available, but the accelerating shift to renewable energy and decarbonization means that those resources are growing less valuable.

Given this challenge, governments should redouble their efforts to develop sectors and industries that generate net value for the economy, have high growth potential, foster innovation, and are resilient to energy price and hazard shocks. These include healthcare, technology, and telecommunications, along with clean energy sectors such as green hydrogen, energy storage, and power generation through renewable sources like wind and solar. These industries create jobs and guarantee successful economic diversification. In that way, they can supplement oil and gas, and make the region more resilient to external shocks.

These industries all require significant innovation and technology. Building them requires a long timeline and a comprehensive approach that touches on different aspects of the economy and society. GCC governments will only succeed when they reduce, or eliminate, the structural barriers to innovation, develop local capabilities, and invest in R&D, among other long-term enablers. More specifically, they should take the following steps:

Build higher-quality infrastructure that supports innovation and technology, particularly in growth areas such as renewable energy and digital infrastructure, and promote competition in the delivery of services to businesses and consumers. Critically, governments should avoid the impulse simply to import technology, and instead embed these capabilities in their countries through sustained initiatives over time.

Reduce regulatory barriers to the adoption of foundational technology, such as drones, artificial intelligence, and advanced analytics. For example, establishing strong data-protection regulations can provide companies with a stable baseline, and ensure that consumers adopt new technologies and keep their data safe.

Attract the right talent by changing the region’s value proposition for global experts. Streamlining immigration policies and reducing the cost of living can bring in talent from around the world, and ensure that they stay long enough to build the domestic talent base.

Improve the quality of local education, with a particular focus on science, technology, engineering, and math (STEM) subjects, along with soft skills such as communication, creativity, and problem-solving.

Encourage the participation of the private sector by creating an ecosystem of innovation. Change banking regulations, revisit existing incentives, and attract new investors such as PE firms to increase funding for promising new ideas and start-up businesses. Encourage companies to launch corporate research functions. Forge alliances between companies and universities. Support the use of M&A, which will allow companies to make faster progress and create a more vibrant market for growing companies when founders want to sell. Rather than individual initiatives, this type of ecosystem approach can become self-reinforcing over time.

GCC governments need to reconsider their economic policy approach. By learning the lessons of the dual shock from COVID-19 and low oil prices, they can take the necessary steps to build economies that are truly diversified, resilient, and based on research and innovation.

This article originally appeared in Gulf Business, July 2020.

Dr. Raed Kombargi, Georges Chehade, and Jorge Camarate are partners, and Jad Moussalli is a principal with Strategy& Middle East, part of the PwC network.

{{item.text}}

{{item.text}}

Menu