The banking landscape in the Gulf Cooperation Council (GCC) region is undergoing a significant transformation with the emergence of regulatory-led open banking initiatives. Open banking involves the consented-to sharing of customer data with trusted third parties, such as other banks, financial technology (fintech) firms, and payment providers. Directives mandating open banking could threaten incumbent banks’ market position. However, with the right vision, these banks can turn that challenge to their advantage. They can retain their market share, redefine their identity, create new revenue streams, and forge deeper relationships with their customers.

Open banking revolutionizes the traditional approach to customer data management and payments in financial institutions.

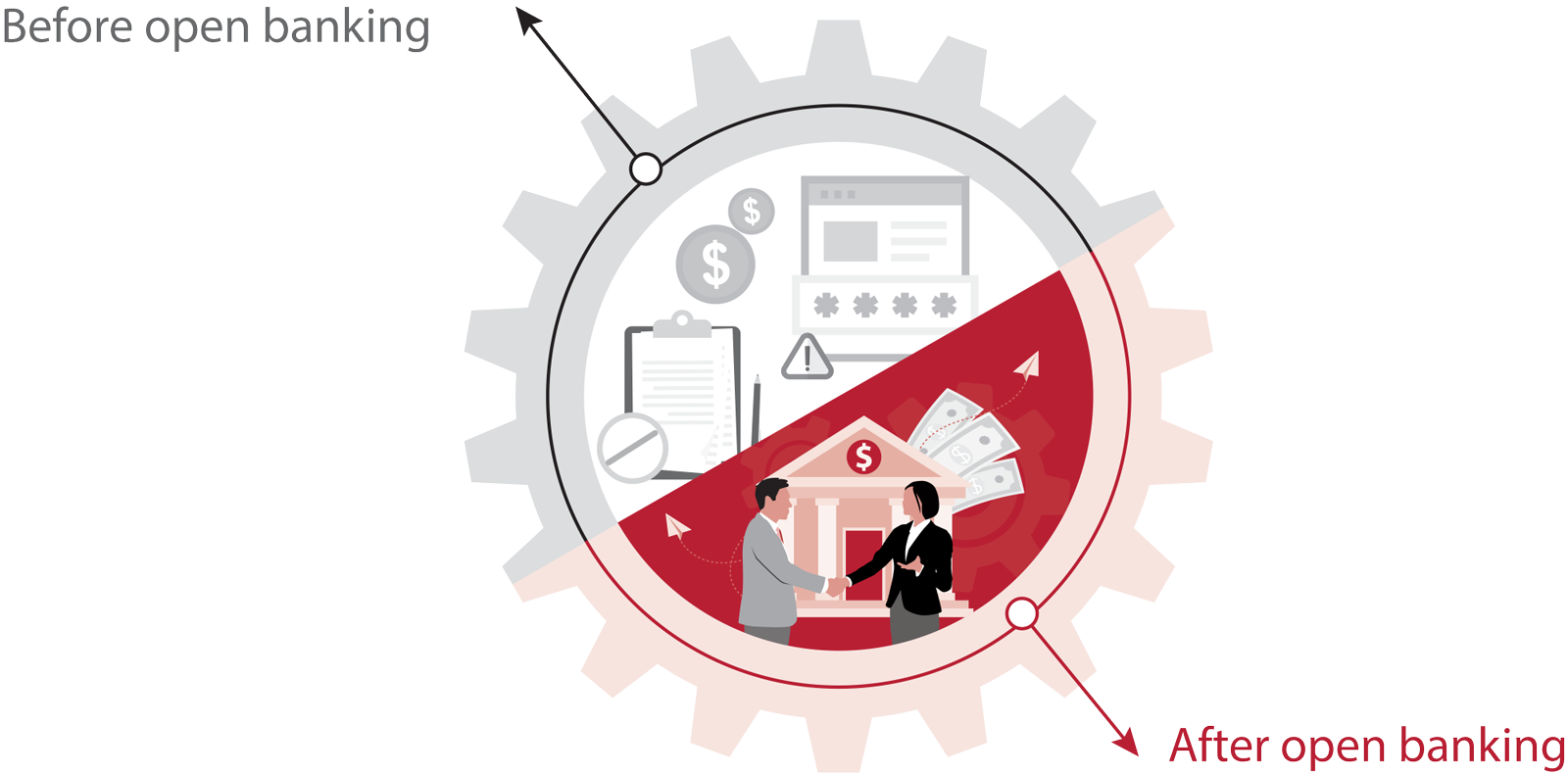

The transformational impact of open banking

End users

- Limited access to their own financial data

- Fragmented experience across different financial institutions

- Concerns about data security and privacy

Data holders (e.g., banks)

- Centralized control over customer data with no legal requirement to share it externally

- Limited interoperability with other financial institutions and service providers

- High costs and complexity associated with integrating third-party services

Service providers (e.g., fintechs)

- High barriers to entry due to integration challenges and lack of data access

- Difficulty in developing innovative financial products and services

- Reliance on manual process and screen scraping for data aggregation

End users

- Greater control over their financial data through standardized permission dashboards

- Enhanced visibility into their financial position across multiple institutions

- Improved access to personalized financial products and services

Data holders (e.g., banks)

- Facilitated data sharing with authorized third parties through standardized APIs

- Enhanced competition and innovation through collaboration with fintechs

- Improved customer experience and retention through expanded service offerings

Service providers (e.g., fintechs)

- Regulatory clarity and compliance through standardized data use and access protocols

- Access to a broader range of customer financial data

- Enhanced customer acquisition, reduced barriers to entry, and faster time-to-market for new products

So, for ambitious banks, the question that prevailed until recently about open banking regulations—“comply or compete?”—is obsolete. These banks can now work on monetizing the disruptive possibilities of open banking by exploiting the capabilities and technologies that they will develop through open banking initiatives. Banks require a playbook composed of three elements that can redefine their identity. Banks can undertake all three of these initiatives simultaneously: power the core, expand revenue boundaries, and transform.

Securing customer consent for data sharing is a crucial step for incumbent banks in defending their market position and preventing the outflow of customer data to competitors in the open banking arena. Without customer consent, banks may be little more than data providers, which their competitors can exploit. With customer consent, banks become consumers of data from external parties, thereby getting to know their customers better and supplying them with financial tools that build loyalty.

Open banking allows banks to expand their revenue boundaries by targeting previously underserved segments and by offering new products, such as premium APIs. The sharing of data provides insights into financial behaviors and personalized risk assessments. Using this information, banks can offer new products tailored to previously overlooked segments such as micro and small enterprises, along with gig-economy workers. Banks also can monetize their data and services through premium APIs and by enabling the broader developer ecosystem. These efforts would target many different kinds of enterprises, including large and established companies that want to improve their efficiency and startups that need premium services to serve their customers better.

Open banking allows banks to acquire new customers and revenues by acting less like traditional financial intermediaries and more like technology companies. One of the most important effects of digitization has been to blur boundaries between industries and allow for new business models. Open banking allows incumbent banks to turn that pattern to their advantage. As incumbent banks accumulate capabilities and expertise, they can break down barriers between industries and help to develop banking-as-a-service (BaaS) and banking-as-a product (BaaP). Such digital offerings would have been unimaginable until recently.

Open banking in the GCC region presents incumbent banks with a chance to go beyond compliance. They can now reinvent their customer relationships and role in the economy by offering their customers tailored products and services. Banks can position themselves for open finance and the open economy. By transforming their approach to markets, they can broaden their scope with new business models and partnerships across industries.

In the news

Open banking is a rich opportunity for GCC incumbent banks

Banking in the GCC region is undergoing a significant transformation with the growing impact of regulatory-led open banking initiatives. The Central Bank of Bahrain is preparing to enter the second phase of its open banking plan. Saudi Arabia has announced the gradual implementation of open banking use cases. Kuwait is testing open banking products, and the Central Bank of the UAE has initiated an open finance initiative covering banks and insurers.

Contact us

Menu