Executive summary

A small number of global marketing agencies have come to dominate their industry after decades of acquiring smaller agencies in a range of specialty disciplines: creative and branding services, digital, media planning and buying, public relations, and market research. Although these subsidiaries are responsible to their parents financially, they otherwise operate independently — and often in direct competition with their sister agencies. That model is breaking. Driven by technological developments, evolving consumer habits, and cost pressures, clients are increasingly seeking unified, best-in-class teams that can work across disciplines and agencies.

The marketing giants have begun to integrate their operations in response to the pressures from clients and the external market. But they aren’t evolving fast enough. They need to fundamentally rethink their organizational structures; become far more integrated across back-, middle-, and front-office capabilities; and play a more active role in day-to-day strategic operations. Here we detail the pros and cons of the four potential next-generation operating models, and offer guidance on determining the best-fit model. The necessary transformations will be disruptive, but each of the risks and challenges of the process contains the potential for opportunities and competitive advantages.

The revolution at hand

The path forward is clear: the rapid development of much more integrated business operating models in which global marketing agencies are not mere holding companies but play a far more active and strategic role — the role, that is, of a true parent company.

There are, of course, a range of ways in which that broad aim might be accomplished. The optimal choices depend on the current status of the parent company’s evolution, its broader strategy, the composition of its client base, and its appetite for change.

We’ll break down the potential choices by where they fall along the spectrum of back- to front-office activities.

Back office

We can address back-office functions quickly because the changes involved tend to be tactical, not strategic, in nature, and because, as discussed above, they amount to table stakes for long-term viability. We recognize that the global marketing companies are already going down this path, but we believe that there is more to be done to drive economies of scale and that the integration needs to be achieved faster.

Transactional back-office activities are the lowest-hanging fruit and should mostly be moved into global shared-services organizations if they have not been already. These include finance functions like accounts payable and accounts receivable; payroll and other transactional HR services; procurement; and nonstrategic IT services. We recommend maintaining a regional or country footprint to serve agencies in each market, but also leveraging offshoring opportunities where possible to create efficiencies.

A range of non-transactional back-office activities and functions are somewhat more strategic in nature but should also be elevated to and managed at the parent level. In this category, talent management is perhaps most critically in need of a company-wide approach. The lack of integrated talent management and succession planning across different agencies means existing agency executives don’t have access to the same opportunities and sponsorship as they would for other massive global corporations. Given the extent to which agencies are suffering from high turnover and losing key talent to tech companies elbowing their way up the advertising food chain, remedying this by taking a top-level approach to talent is paramount. Other functions in this category include the strategic capabilities around treasury, tax, legal, and governance.

Middle office

The next stage of this transformation involves non-client-facing capabilities that nonetheless directly support front-office functions and tend to be strategic in nature. These capabilities should be either elevated to the parent-company level or housed in a single agency or business unit that would serve as a center of excellence (COE) for the other agencies.

Production services may be the most urgent focus in this category because they sit at a collision point between so many different market dynamics — in particular, the need for more content across more media and platforms, often without additional budgets. As a result, clients are increasingly asking for cost transparency, visibility into production supply chains and vendor relationships, and demonstration of the careful stewardship of client budgets. All this argues for the consolidation of agency production services to generate demonstrable production efficiencies through best practices like price normalization, project bundling, talent resource management, volume discounts for commodities such as travel and equipment, and consistent client reporting and analysis.

Other important middle-office functions that should become shared capabilities include data management and privacy, both critical capabilities for data-driven marketing.

Front office, go-to-market capabilities, and fundamental business unit structures

If there is any lingering doubt that client-facing services (and not just back- and middle-office functions) need to undergo a similar movement toward centralization, let the following anecdote dispel it.

For an important recent presentation to a major global consumer-products manufacturing client, one of the global marketing companies assembled a multidisciplinary team of all-stars from across its agency network. It was a clear effort to both dazzle the client with the assembled talent and demonstrate that it could marshal an integrated best-in-class, cross-agency team on the client’s behalf.

The move backfired, however, when the client noticed that members of the cross-agency team were introducing themselves to one another before the meeting, and in some cases couldn’t distinguish between the client executives and their sister-agency counterparts. The next day, the client engagement was formally terminated.

The lesson: Superficial change, characterized by ad hoc task forces being grafted atop the existing operating model, isn’t going to work. On the other hand, meaningful change that will better position the marketing giants strategically is a matter of not just regrouping functions but fundamentally rethinking organizational and operational structure to better serve clients. Existing agency brands can’t emerge from this process untouched, and new business units will need to be formed.

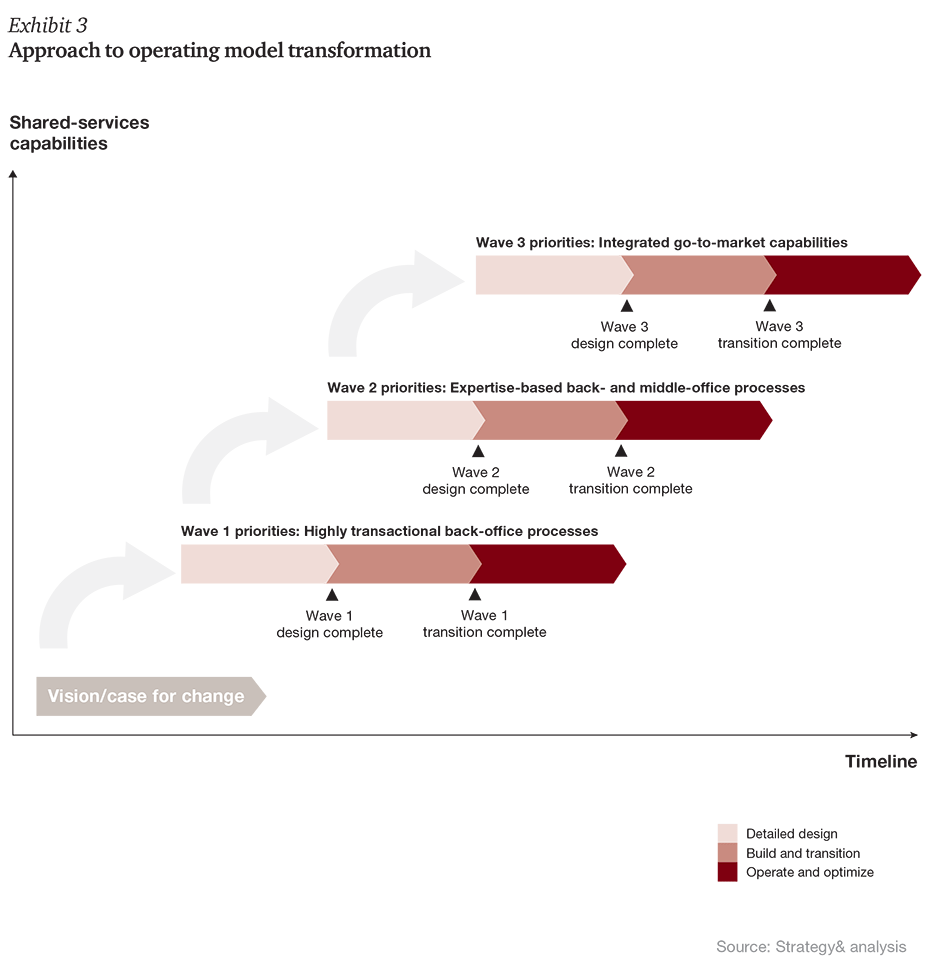

Getting started

To make it work, a phased transition road map needs to be planned meticulously. The plan should start by communicating the vision and roll-out process at an increasing level of detail. The iterative approach described below should minimize business disruption and help ensure stakeholder alignment.

Companies need to conduct a top-down assessment across the portfolio of businesses and develop a long-term operating model strategy for the company. Doing so is the key first step to develop the longer term vision and identify waves of execution that can minimize business disruption.

We see three potential waves of execution.

Wave 1: Integrate highly transactional back-office capabilities, including finance, payroll, and other HR transactions; IT; and procurement.

Wave 2: Tackle non-transactional, expertise-based back- and middle-office activities, including talent management, data management, and privacy and policy.

Wave 3: Begin the integration of brands into business units, by local hub or by country or by agency.

None of these transformations will be easy. Global marketing companies, after all, have been paying lip service to many of these ideas for years — but for a variety of reasons are not yet “walking the talk” in terms of unifying agencies across similar disciplines. And, with a few isolated exceptions, they have barely scratched the surface on the concept of collapsing agencies from different disciplines into a single multidisciplinary business unit.

To be sure, the risks of these changes are high, but the potential benefits are also high. Integration provides more growth potential for talent and better retention for the company. It generates efficiencies of scale. It makes the company better able to integrate future acquisitions. It reduces complexity, increases speed-to-market, and cleans up incentives. And, perhaps most important, it creates opportunities for better pricing models, heftier margins, and substantial earnings expansion.

Contact us